The sustainability trend has been prevalent across all sectors for some time now. However, the omnipresent threat of climate change, along with the associated environmental changes and social upheaval, provide emphatic proof that the topic has long since progressed beyond a passing fad and should instead be regarded as a comprehensive and ongoing development.

Indeed, the ESG-based approach – which covers environmental, social and corporate governance criteria – is far more than simply a greenwashing tool for financial institutions to polish their image. Almost all banks have now begun to include ESG-related matters in the course of annual reports or in their own reporting formats. Sustainability ratings, such as those published by ratings agencies like Vigeo Eiris, play an increasingly important role in bank refinancing processes. Demand for sustainable financial products and investments is rising and EU authorities are continuously revising and refining the regulatory framework on ESG. This is giving rise to new requirements that banks will struggle to meet without digital support.

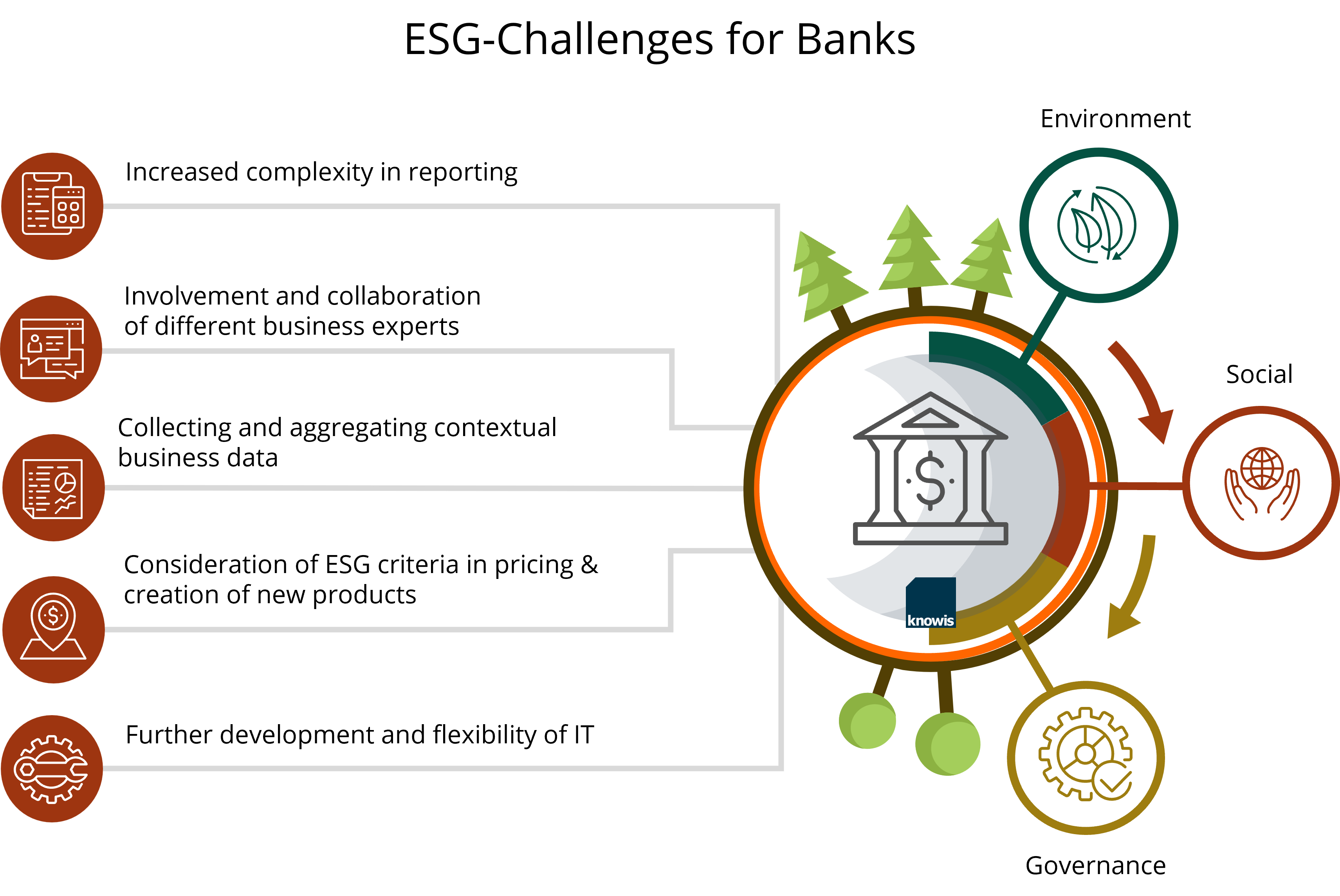

Regulatory systems: ESG reporting creates added complexity

In Germany, most banks are obligated to publish sustainability reports in line with the CSR Directive Implementation Act (CSR-RUG). In doing so, they must adhere to the requirements of the Non-Financial Reporting Directive (NFRD), which requires the publication of information on environmental, social and employment matters. The need for measures to uphold human rights and counter corruption are also becoming vital topics. In relation to environmental protection, financial institutions disclose details such as how they are contributing to the fight against climate change and what measures they have in place to monitor their customers’ and suppliers’ ecological footprints. One example would be the energy efficiency of buildings, which is a vital consideration in real-estate financing.

Banks are increasingly looking to finance sustainable lines of business. The extent to which a business activity is considered sustainable is regulated by the EU taxonomy. This regulation is already in effect in simplified form and will increase considerably in scope and specificity in 2024. The Corporate Sustainability Reporting Directive (CSRD) is also likely to come into force the same year. This ties in with the EU taxonomy and will replace the NFRD. The EU Commission hopes that this legislation will create uniform EU standards.

The key ESG requirements: How software can reduce complexity

An examination of the current regulatory system shows that ESG is a demanding topic with many obvious requirements and implications for banks. However, some of its effects are not yet sufficiently clear or understood. By highlighting a few topic areas, we will demonstrate how the use of modern software can help institutions to manage ESG requirements more effectively.

Smart collaboration

ESG requirements cover all areas of banking and therefore require intensive collaboration between specialists from many different departments. These staff are generally already subject to considerable pressure in their day-to-day duties, so want to be integrated in ESG processes through modern, smart systems – without an avalanche of paperwork, emails, or time-consuming coordination phases.

Solution: A digital expert workplace

The user logs into their own digital workplace. The system informs them of the tasks they have been assigned in line with their roles and authorizations, and provides the context required to complete them. A configurable dashboard, task lists and boards are all available to organize the user’s work and facilitate collaboration with other users.

Managing business data

ESG requires financial institutions to record, manage and aggregate new business data. This data comes from very different domains and is sometimes generated in the course of project processing, such as on financing projects. Implementing corresponding data fields in core systems presents a challenge, while managing the authorizations of all current and future users is also complex. In addition, media discontinuities occur when business data is “scattered” across fragmented applications and therefore needs to be manually aggregated and transferred into reports. Taxonomies and assessment requirements need correspondent and coherent business data.

Solution: Context-based and future-focused data management

In the context of ESG, the focus is increasingly shifting from solely determining absolute values and instead considering relative effects on other contexts. In concrete terms, this means that a positive attribute in one ESG-related field must not have a negative effect in another field. Instead, the various topics of ESG must be viewed together as a whole.

This integrative approach requires data models that are based on factual realities and can be created and amended in straightforward processes by the relevant specialists. The ESG criteria set down in regulatory frameworks will also continue to evolve and, in turn, require IT solutions to adapt. The overall topic of data management has extensive consequences, as ESG requires more than just reporting – it requires constant monitoring.

ESG and compliance

The consideration of ESG-related criteria is evolving beyond a “simple” reporting obligation and is instead becoming relevant to auditing processes. Instead of a simple “yes” or “no” structure, the structure of ESG reporting is increasingly shifting towards examining the plausibility, adequacy and conformity of the reported data. As a result, financial institutions are now obligated to document not only what they do in relation to ESG topics but also how they do it. This is relevant for various processes and procedures including external audits, extraordinary audits, and internal administrative audits.

Solution: Logging, authorization, documentation via one software solution

Working with modern, industry-specific software makes it possible to implement need-to-know systems and authorization access controls, ensure data security, record and document user access, and keep track of completed tasks and recorded data out of the box. This significantly simplifies and reduces the work needed to ensure adherence to compliance requirements. Users can also be given tools and references to written rules of procedure within outstanding tasks.

Flexibility & development

Banks regard ESG not as a project but as a continuous, and ongoing program. As noted above in the section on data management, this means it is vital that any solutions can be adapted accordingly. This requires a flexible software architecture that focuses on specialist domains and supports users with appropriate customization.

Solution: Integrating everyone involved

“Democratization of technology” is often used to describe a situation in which all actors can be integrated into a technological system in line with their needs and skills. Institutions need the energy and expertise of numerous actors to successfully implement ESG program.

This relates in particular to specialist departments where staff need to model and configure ESG-related subject matter in no-code processes. However, institutions also need IT-adjacent teams that can rapidly implement user interfaces, business logic and actions using low-code solutions – that is, software with simplified programming requirements. However, there are also certain requirements of such complexity that IT specialists have to take care of them, who can perform pro-code development in their preferred programming language.

This relates in particular to specialist departments where staff need to model and configure ESG-related subject matter in no-code processes. However, institutions also need IT-adjacent teams that can rapidly implement user interfaces, business logic and actions using low-code solutions – that is, software with simplified programming requirements. However, there are also certain requirements of such complexity that IT specialists have to take care of them, who can perform pro-code development in their preferred programming language.

A modern software solution can facilitate this and ultimately does not distinguish by how individual modules were developed.

Conclusion

Many aspects of ESG remain in their infancy. However, it is already clear that the new requirements in store for financial service providers will require significant engagement. ESG is certainly not a topic that a single unit can handle alone; instead, it needs specialists in various departments to collaborate intelligently. This means it is also a particularly relevant topic for digitalization initiatives.

Will there be specific standards in the future – and therefore standard solutions? This will presumably happen in time in some areas. However, there is a great deal more evidence that there will be a high degree of individuality based on individual institutes’ business models and contexts. That fact that specialist and regulatory requirements will continue to develop in future is a key argument in favor of selecting a flexible, open IT solution in the context of ESG.

You have questions, suggestions or want to contact us? Use our contact form to get in touch with us. We are looking forward to hearing from you.

Teaser image: Orbon Alija – iStock – 464671522.

Infographics: knowis AG.